The risks facing the European real estate market in the coming months

Demand for new housing is being affected by rising interest rates and inflation, and margins are being squeezed by construction costs, predicts S&P.

Property developers and builders across Europe should prepare for challenging times. According to S&P, several external factors are likely to impact the new construction sector over the next 12 to 18 months. Rising interest rates, inflation, and energy costs stemming from the Russo-Ukrainian conflict could have repercussions for the European real estate market.

Interest rates and inflation: how they affect the housing market

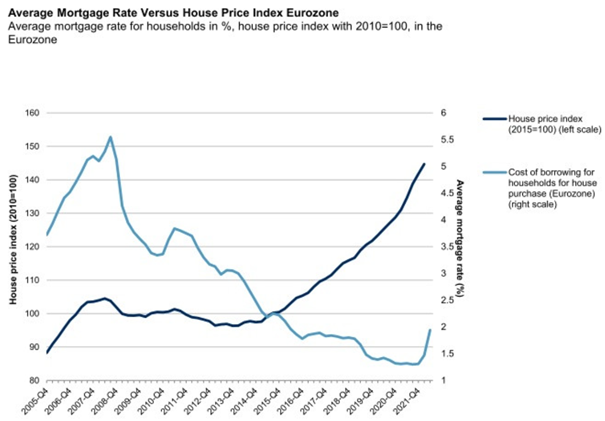

According to S&P, current conditions could lead to a decline in sales volume. The market is heavily reliant on mortgages (70% of newly built homes in Europe are financed with home loans), which are influenced by interest rates and lending conditions.

Uncertainty may lead families to postpone buying a new home, as rising property prices, linked to inflation, and the increased cost of living are not accompanied by a rise in real wages. Portugal, for example, has the largest gap between housing prices and wages in the OECD, with housing costs exceeding labor income by 47.1% in the first quarter of 2022.

In addition, the conflict between Russia and Ukraine, as well as problems in the global supply chain, are leading to increased costs and shortages for builders, which may delay and make projects more expensive.

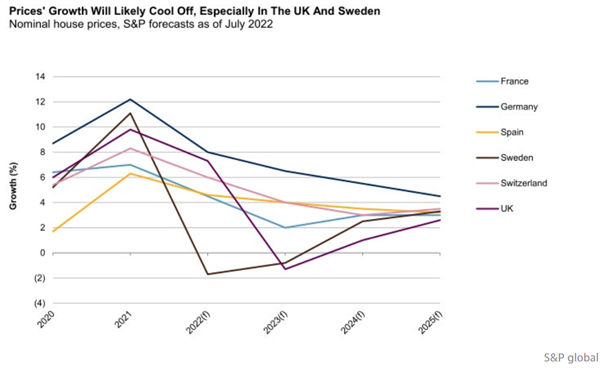

Housing prices in Europe

To maintain profit margins, S&P states that cost optimization plans and strong cash reserves are necessary. Furthermore, among the factors driving prices is a shortage of new housing. In Portugal, for example, demand for real estate relative to supply has caused housing prices to skyrocket in recent years.

Forecast on European real estate

Here are the main trends identified by S&P for the coming months in the new construction sector:

Rising interest rates and weakening purchasing power are expected to reduce demand for new housing in Europe, a market that relies primarily on mortgage loans, even if government incentives can act as a stimulus.

In addition, rising construction costs, energy costs (which account for 5 to 10% of price increases), labor shortages, land scarcity, and supply chain problems continue to hinder the delivery of housing units.

Stricter environmental and safety requirements are driving demand for new construction, but are also resulting in additional costs and technical challenges for builders.

It is therefore expected that during the last quarter of the year, European property developers and builders will already begin to experience increasing pressure on revenues and margins, as it will be difficult to pass on the increase in costs to end customers.

The bulk of the impact is not expected to be felt until 2023. However, most European property developers rated by S&P should overcome the obstacles and maintain credit parameters in line with annual ratings, thanks to strong balance sheets and good levels of liquidity.