IMPORTANCE OF THE CHOICE OF LEGAL STRUCTURE

In the context of an inheritance or sale of a business, the tax consequences can hold some unpleasant surprises.

A skilful structuring makes it possible to carry out a succession, sale of company exempt from taxes or at least optimized on the tax plan.

The choice of a company's legal structure is too often overlooked from the outset.It is not uncommon to find that people only start to worry about it when the company is being sold, and unfortunately, it is often too late to act and make the necessary changes for a favorable final tax situation.

Consequently, a large number of owners of small SMEs for whom this sale often represents the capital used to finance their retirement realize that once the taxes and duties have been paid, the balance will not be enough to achieve their goal.

If the seller's legal structure is a sole proprietorship or a general partnership, thecapital gain from a sale of a company (i.e., the difference between the price paid by the buyer and the book value of the company) will be subject to income tax and social security contributions in addition to other income in the year of the sale, which, depending on the individual's private tax situation, amounts to charges of up to 50% of the sale profit.

- Taxation when selling a business in Switzerland?

The tax rate on the sale of a business can vary between 0% and 50% depending on the structure of the transaction.

The elements that determine this rate are:

- The legal structure of the Seller (i.e., SA, Sarl or partnership)

- The Buyer's legal structure

The taxation of a business transfer will differ depending on whether the seller and/or buyer is a sole proprietorship (i.e., a sole proprietorship or general partnership) or a corporation (i.e., a public limited company or a limited liability company )

2 - Potential taxes when selling a business?

1. Capital gains tax on the sale of a company (i.e., for partnerships)

2. Indirect partial liquidation (i.e., for public limited companies (SA) and private limited companies (SARL))

3. Transfer of ownership (i.e., for public limited companies (SA) and private limited companies (SARL))

These taxes can be avoided with the right legal structures and tax and financial preparation prior to a business sale transaction.

3 - Minimize taxation when selling a business?

It is essential and essential to put in place the right legal structures from the start!

A financial preparation upstream can allow you to avoid paying any tax!

- Prepare the legal and financial structure ahead of the sale to minimize taxation when selling a business.

- Negotiate the legal structure that the buyer will use to buy you out, as this may trigger other taxes (eg indirect partial liquidation)

The Swiss tax authorities may require 5 years before recognizing your new structure if necessary!

4 - Howto avoid capital gains tax?

Capital gains from the sale of a company or the transfer of shares in a holding company will not be taxed in the same way depending on the legal structures of the parties involved in the transaction. A corporation (i.e., a public limited company, a private limited company) will be exempt from capital gains tax, while a partnership will be subject to this tax. it is important to convert your business into a corporation when selling a company with a significant capital gain.

5 -Taxes applied in the different scenarios

- Sole proprietorship or partnership sale

collective

If the seller's legal structure is a sole proprietorship or a general partnership, the capital gain from the sale of a company (i.e., the difference between the price paid by the buyer and the company's book value) will be subject to and treated as income tax. Social security contributions (10%) will also be payable.

Sole proprietorships and general partnerships are therefore unsuitable structures for minimizing taxes on the sale of company shares. One solution is to convert the partnership into a corporation (i.e., a public limited company or a private limited company). This must be done five years before the actual sale of the company for the tax authorities to recognize the new structure. Selling your company with the lowest possible tax burden therefore requires using a different legal structure.

CONCLUSION – PARTNERSHIPS ARE AN INADEQUATE FORMAT AT THE TAX LEVEL FOR THE TRANSMISSION OF BUSINESSES IN SWITZERLAND

- Capital company – SA or Sarl

A capital company (ie SA or Sarl) benefits from an exemption from capital gains tax in Switzerland.

This means that no tax has to be paid on the capital gain of the shares/shares of the company when the SME is sold.

However, there is one scenario where capital gains tax is still payable. If the seller owns the company privately and the buyer is a legal entity (i.e., a company), this can lead to "indirect partial liquidation," which may generate tax payments after the sale (i.e., as described below).

B1. The buyer is a natural person

If the company being sold is a corporation privately owned by an individual, and the buyer is also an individual, no capital gains tax will be payable on the sale of the company. Therefore, taxation on the sale of a business is not an issue in this case.

B2. The buyer is a legal person (ie company)

If the company being sold is a capital company owned by a natural person and the buyer is a legal entity, two elements may apply: "Transposition" and "Indirect Partial Liquidation".

.

"Indirect partial liquidation" stipulates that taxes may be required from the seller after the sale of the company in the event of the presence and distribution within 5 years of excess reserves (eg large cash reserve in the company) in the company sold.

In this situation, capital gains are considered taxable income (and no longer exempt).

In order to avoid being in this business sale tax situation, transaction structures can be put in place by merger and acquisition advisors.

B2.1. What are the conditions for being in an indirect partial liquidation situation?

- The sale involves a stake of at least 20%.

- The transfer of shares leads to their passage from the private fortune of the seller to the commercial fortune of the buyer.

- There are distributions of excess reserves (eg dividend greater than annual net income) within 5 years after the sale of the company

B2.2. Transposition, how does this impact the tax on the sale of a company?

Transposition is the act of transforming taxable (excess) reserves into non-taxable reserves.

As an example, imagine that a company has 100 of taxable excess cash and the new owner replaces this cash with a financial participation of another company. This transaction would allow the initially taxable amount (ie cash) to be replaced by a non-taxable amount (ie the new financial participation).

To compensate for this mechanism, the tax administration taxes this type of "transposition" as returns of fortunes. In order to avoid being in this tax situation, transaction structures can be set up by merger and acquisition consultants for SMEs.

C – Capital company – Real estate company SA or Sarl

A real estate company (SI) in Switzerland is a form of company, generally anonymous, whose corporate purpose is specifically the investment, construction and operation of buildings.

If the company for sale qualifies as a real estate company, the sale represents a transfer of economic ownership and lods and sales duties, as well as real estate gains taxes, are applicable.

6 – Donation subject to reservations

If shares are sold to a general partnership, to former or new partners, the difference between the market value and the actual (too low) selling price may be considered a gift and gift tax may be levied accordingly.

Some cantons have a massive exemption from inheritance or gift tax in the context of business successions to tax-exempt recipients or heirs, such as e.g. the canton of Zurich which exempts at 80%.

However, depending on the canton, a period of between 5 and 15 years must be taken into account, during which the establishment must retain its corporate name or a majority stake must remain.

7 – Donations and legacies

In almost all cantons, donations and inheritances to direct descendants are exempt from gift and inheritance taxes.

If inheritance within the family (particularly to children or grandchildren) is planned, thesole proprietorship, partnership interest, or shares in corporations can be gifted or bequeathed tax-free. The donor or the deceased also suffers no tax consequences in this case.

In principle, this exemption also applies to property taxes (lods duty and real estate sales and gains taxes), insofar as real estate is involved.

In the case of an internal succession within the family, the aspects of the law of succession (protection of the reserved part of the heirs who are not successors) must be taken into account. In some cases, a non-taxable division of the business into two (or more) parts of establishment is necessary for this purpose.

If succession within the family should not be carried out graciously, but facilitated by a reduced sale price, the company can be "lightened" in two ways: on the one hand, if this also proves less attractive from a tax point of view, by the withdrawal of resources unnecessary for the operation of the company or, on the other hand, by the repurchase of own shares (up to 10%) at their market value, which must be resold within 6 years.

For reminder and information

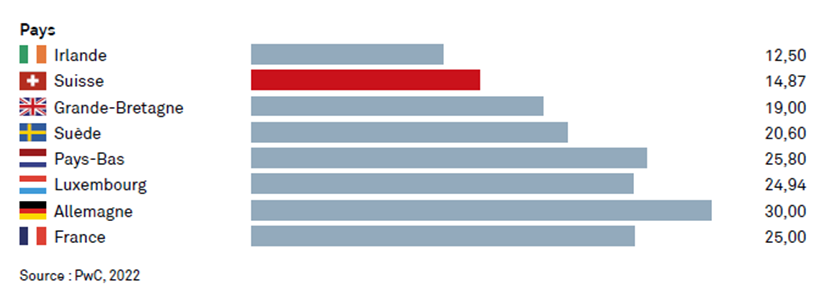

Corporate tax in Europe

VAT in Europe

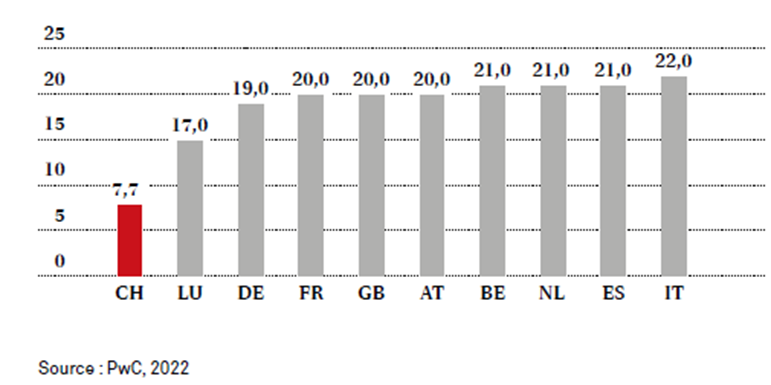

Tax shares in Europe

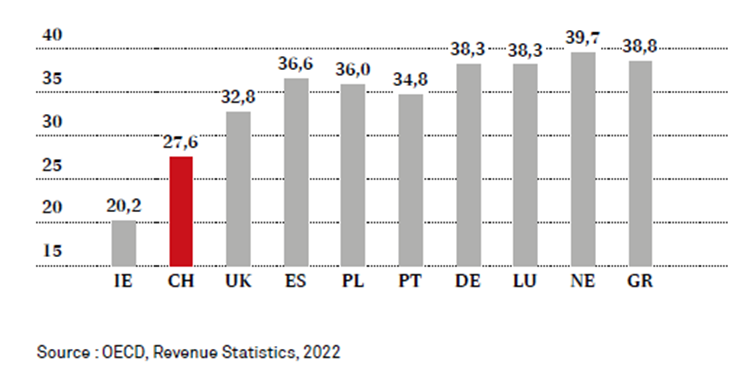

Taxes and contributions to social insurance 2020 in relation to GDP (in %)