The real estate market is easing. Swiss mortgage rates are falling

The decline in inflation leads to a decrease in interest rates, particularly those applied to construction.

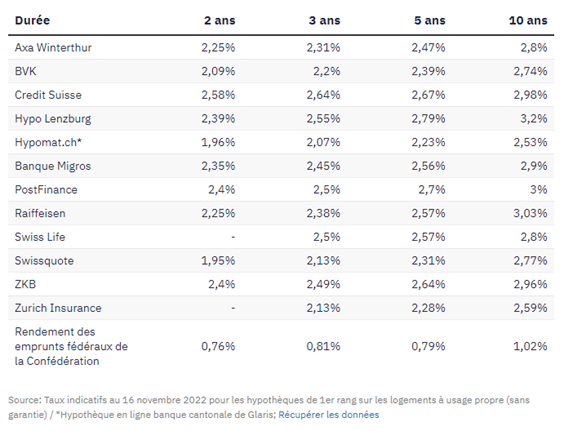

Over the past four weeks, mortgage rates have fallen significantly in Switzerland. All twelve lenders whose indicative rates for fixed-rate mortgages are regularly collected by the magazine "Finanz und Wirtschaft" have lowered their rates, sometimes considerably. All loan terms are affected.

For ten-year terms, indicative rates have fallen by an average of 0.38 percentage points. The Zurich Cantonal Bank and Swiss Life have lowered their rates by 0.46 percentage points for ten-year fixed-rate mortgages. Zurich Insurance has even reduced its indicative rate by 0.48 percentage points for five-year mortgages. By comparison, the average market decrease is 0.32 percentage points for a five-year term.

Fixed mortgage rates in %

Mortgage interest rates of 3% or more for ten-year contracts seem to be a thing of the past, at least for now.

Last month, all but one institution still required rates of 3% or more. Now only three do: Hypo Lenzburg, Raiffeisen, and PostFinance.

Rates below 2% are once again possible for short-term loans. These are offered by Swissquote and the online platform Hypomat, which is backed by the Glarus Cantonal Bank.

Inflationary pressure is decreasing

The general downward correction indicates that the inflationary environment has eased. In Switzerland, the annual increase in consumer prices fell in October for the second consecutive month, reaching 3%. This remains well above the Swiss National Bank's price stability target of 2%.

Last week, National Bank President Thomas Jordan reiterated that the key interest rate is expected to be raised again in December. However, inflation is on track as predicted by the custodians of the currency, who anticipate a decline to 2% and even lower next year. The pressure to set the key interest rate significantly higher is therefore easing.

It remains to be seen whether today's significant drop in mortgage rates truly represents a trend reversal. Following the correction in July, this is only the second monthly downward adjustment this year. Overall, ten-year mortgages are still more than twice as expensive as they were at the beginning of the year.

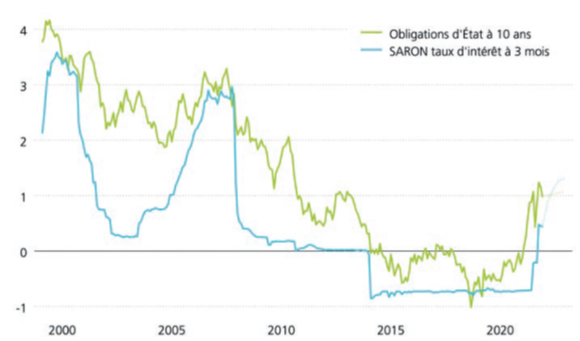

SARON 3-month returns and 10-year actuarial returns, expressed as a percentage

Market expectations regarding interest rate trends are reflected in the futures markets.

According to forecasts, short-term interest rates measured by the 3-month SARON in Switzerland are expected to rise by 0.75 percentage points over the next twelve months.

If this hypothesis is confirmed, the cost of Saron mortgages will also increase by 0.75 percentage points. However, it is long-term fixed-rate mortgages that have seen the largest rate increase, as they align with the evolution of long-term rates in the capital markets.

Global economic data

Source: Bloomberg – Finanz und Wirtschaft.