The revision of inheritance law will come into effect on January 1, 2023

CHANGES AS OF 01.01.2023

https://www.admin.ch/gov/fr/accueil/documentation/communiques.msg-id-83570.html

At its meeting on May 19, 2021, the Federal Council decided that the revision of the law of succession would come into force on January 1, 2023.These new provisions will allow testators to freely dispose of a larger part of their assets.

The new inheritance law will be more flexible. Testators will be able to freely dispose of a larger portion of their assets.

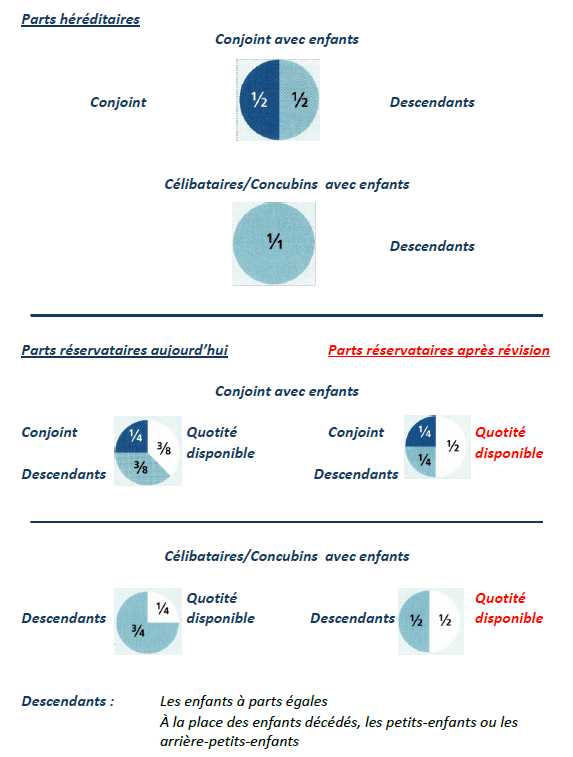

Currently, the children's reserved portion of the estate is equal to three-quarters of the legal share. In the future, it will be reduced to half. The parents' reserved portion, however, is being completely abolished.

The rights of the spouse or registered partner, however, remain unchanged. A person wishing to settle their estate by will will be less constrained by the forced heirship rules. They will be able to dispose of their assets more freely and, for example, favor their common-law partner more. The Federal Council has decided that the revised inheritance law will come into effect on January 1, 2023.

The transfer of a business will also be made easier.

Definitions and explanations

To better understand this case, here is some explanation of the legal terms used in inheritance law

Legal heirs

The legal heirs are those designated by law to inherit if the deceased did not express a last will and testament.

Inheritance rights vary according to the civil status of the deceased at the time of death and the degree of kinship of his survivors.

Legal heirs inherit according to a certain order of succession based on the degree of kinship or, more precisely, according to the order of kinship with respect to the deceased.

The closest relatives exclude those who are more distant. Therefore, the legal heirs are always those of the closest relatives.

The first group of relatives consists of the deceased's direct descendants, namely his children or their descendants. The children inherit in equal shares within each branch.

Adopted children or natural children inherit in the same way as legitimate children;

The second kin inherits when there are no descendants left. It includes the father and mother or, in the event of predecease, the brothers and sisters of the deceased or even their descendants if one of them has predeceased them;

The third group of relatives consists of the grandparents and their descendants. These include uncles and aunts, cousins, or their descendants.

The surviving spouse is outside the family circle since he/she is not related to it by blood.

Certain close relatives are legally entitled to a specific proportion of the inheritance. These forced heirs are:

The surviving spouse

The descendants

Inheritance share

The legal inheritance share is the portion of the inheritance to which a person is entitled by law, unless the testator has decided otherwise (e.g., with a will).

Reserved inheritance

The reserved portion is the minimum share of the inheritance, defined by law, to which a person is entitled; it is less than the statutory share. However, not all legal heirs are entitled to a reserved portion.

Only the spouse and children of the deceased are entitled to a mandatory share

If a will does not respect the reserved portion of the estate, it is not automatically void; it must first be contested by the legal heirs.

Available quota

The disposable portion is the share of the estate that remains after deduction of the reserved portions. The testator can bequeath this portion as they wish, to individuals or non-profit organizations, by means of a will or a succession agreement.

Swiss Will

The Swiss Civil Code provides for three forms of will: holographic, public, and oral. The holographic will is the simplest and most common form. It must be entirely handwritten, dated, and signed by the testator.

Swiss Inheritance Pact

A succession pact is a contract between two or more persons whose object is the succession of at least one of them.

Any person capable of discernment and aged 18 years or over may enter into a succession agreement.

With the agreement of the heirs, the testator can freely dispose of their estate without limit. For example, a forced heir can renounce all or part of their inheritance through this act.

The inheritance agreement may infringe upon the reserved portion of other heirs who are not participating in the contract.

In this case, the injured parties can assert their rights through an action against the other heirs (action for reduction).

The inheritance agreement is established in authentic form (before a notary).

Unlike a will, a succession agreement cannot be unilaterally modified. Any change must be made in the presence of a notary and with the participation of all parties

Changes for married couples

- The inheritance rights of descendants will decrease.

- Today, children are entitled to a reserved portion of 3/8 of their inheritance.

- From now on this share will amount to 1/4. The disposable portion will increase from 3/8 to 1/2.

- The testators will therefore be able to dispose of a larger share of the inheritance as they see fit

- Married couples living in a blended family will be able, thanks to the increase in the disposable portion, to favour their own children, but also to take into account their stepchildren.

- Spouses can better protect each other. This is especially important when the surviving spouse is dependent on income from the estate or must pay off the mortgage to keep their home.

- Otherwise, he will at worst be forced to sell in order to reduce his fixed costs or to compensate the children.

- A reduction in the reserved portion of an estate allows business leaders to more easily settle succession within their company.

Changes for unmarried partners

- Inheritance law does not regulate cohabitation.

- Without specific provisions, cohabiting partners and their children will therefore not be able to claim inheritance even after the revision of inheritance law.

- Since these constellations can be very different, it is not the law but the testators who, even after the reform, will remain empowered to decide which people they wish to favor.

- In the future, testators will have more leeway to do this, as the inheritance rights of descendants will decrease and those of parents will disappear entirely.

- Cohabiting partners and blended families must also take steps to avoid an unfair situation when dividing an inheritance.

- Anyone who has already settled their estate and drawn up, for example, a will should study with an independent specialist the points that need to be adapted due to the reform in order to avoid making mistakes.

Loss of the right to a reserved portion of the estate during divorce proceedings

Divorced spouses whose divorce decree is enforceable lose all rights to the other's estate; this also applies to registered partnerships.

The surviving spouse and registered partner currentlytheir right to the inheritance share and the reserved portion if the other spouse or partner dies during divorce proceedings.

Today, registered partners and married couples are equal before the law. With the revision, the spouse and the registered partner will lose their right to a reserved portion of the estate as soon as divorce proceedings are filed.

Until the divorce judgment is enforceable, the surviving spouse and registered partner will still be entitled to their legal inheritance share unless the testator has decided otherwise (e.g. through a will).

Changes, transmission of a company

- Passing the business on within the family is much more than just a legal challenge.

- Simply favoring or disfavoring one family member over many others can harm family relations and generate multiple problems for the new owner.

- Under the new inheritance law, the reserved portions constitute a smaller share, which facilitates transmission within the family.

Prospects for future review stages for family businesses

- In a future stage of the revision of inheritance law, it is planned to facilitate the transfer of family businesses.

- Family businesses are particularly threatened in the event of the owner's death if their estate is not settled.

- Depending on the valuation of a company, its buyers must pay high compensation to their co-heirs who are protected by inheritance reserves.

- This can put a company in difficulty or even lead to its fragmentation if a large part of the assets are tied up in the company.

- The revision aims, among other things, to allow the deferral of payment of compensation if the company has insufficient liquidity for an immediate payment.

Legal inheritance shares, reserved portions and disposable portion

SWISS CIVIL CODE – INHERITANCE LAW

RO 2021 312 OF 18 December 2020 – ENTERING INTO FORCE ON 1 JANUARY 2023

Schweizerische Bundeskanzlei / Kompetenzzentrum Amtliche Veröffentlichungen (KAV)

Swiss Civil Code

(Inheritance Law)

Update of December 18, 2020

The Federal Assembly of the Swiss Confederation,

Having regard to the message from the Federal Council of 29 August 2018[1],

stop:

I

The Civil Code[2] is amended as follows:

Article 120, paragraphs 2 and 3

2 Divorced spouses cease to be each other's legal heirs.

3. Unless otherwise stipulated, the spouses lose all benefits resulting from testamentary dispositions:

1. at the time of the divorce;

2. at the time of death if divorce proceedings resulting in the loss of the surviving spouse's reserved portion are pending.

Article 216, paragraphs 2 and 3

2 The participation in the profit allocated in excess of half is not taken into account for the calculation of the inheritance reserves of the surviving spouse or registered partner as well as of the common children and their descendants.

3 Such an agreement cannot infringe upon the reserved portion of children from a previous relationship and their descendants.

2 The same applies in the event of dissolution of the regime due to death, when divorce proceedings resulting in the loss of the surviving spouse's reserve are pending.

Art. 241, para. 4

4 Unless otherwise stipulated in the marriage contract, the modification of the legal division does not apply in the event of death when divorce proceedings resulting in the loss of the surviving spouse's reserved portion are pending.

Art. 470, para. 1

1. Anyone who leaves descendants, their spouse or registered partner has the right to dispose of what exceeds the amount of their reserved portion upon their death.

Art. 471

| II. Reserve |

The reserved portion is half of the inheritance tax.

Art. 472

| III. Loss of the reserved portion in the event of divorce proceedings |

1. The surviving spouse loses their reserved portion if, at the time of death, divorce proceedings are pending and:

1. The proceedings were initiated by joint application or continued in accordance with the provisions relating to divorce by joint application, or

2. The spouses have lived separately for at least two years.

2 In such a case, the reserves are calculated as if the deceased had not been married.

3 Paragraphs 1 and 2 apply by analogy to the procedure for dissolving a registered partnership.

Art. 473

| IV. Usufruct |

1 Regardless of how the disposable portion is used, the spouse or registered partner may, by disposition in cause of death, leave the survivor the usufruct of all the share devolving to their common descendants.

2. This usufruct serves as the inheritance right granted by law to the surviving spouse or registered partner in conjunction with their descendants. In addition to this usufruct, the disposable portion is half of the estate.

3. If the surviving spouse remarries or enters into a registered partnership, their usufruct ceases to encumber, for the future, the portion of the estate that, at the testator's death, could not have been the subject of the bequest of usufruct according to the ordinary rules on the reserved portion for descendants. This provision applies by analogy when the surviving registered partner enters into a new registered partnership or marries.

Art. 476

| 3. Life insurance and related individual pension plans |

1 Death insurance policies taken out on the life of the deceased, including within the framework of linked individual insurance, which he contracted or disposed of in favour of a third party by inter vivos act or on account of death, or which he transferred free of charge to a third person during his lifetime, are added to the estate only for the surrender value calculated at the time of death.

2. The claims of the beneficiaries resulting from the individual pension plan of the deceased with a banking foundation are also added to the estate.

Art. 494, para. 3

3. However, testamentary dispositions and inter vivos gifts that exceed customary gifts may be challenged to the extent that:

1. where they are incompatible with the commitments arising from the inheritance agreement, particularly when they reduce the benefits resulting from the latter, and

2. where they were not reserved in this pact.

Art. 522

| B. On the action for reduction I. Conditions 1. In general |

1. Heirs who receive an amount less than their reserved portion have the right to bring an action for reduction, until the reserved portion is restored, against:

1. Acquisitions by reason of death resulting from the law;

2. Gifts made in contemplation of death, and

3. Gifts between living persons.

2. Provisions made in contemplation of death relating to the shares of legal heirs are considered to be simple rules of partition if they do not reveal a contrary intention on the part of their author.

Art. 523

| 2. Reservation holders |

Acquisitions upon death resulting from the law and gifts upon death benefiting the forced heirs are reducible proportionally to the amount that exceeds their reserved portion.

Art. 529

| 4. Life insurance and related individual pension plans |

1 Death insurance policies taken out on the life of the deceased, including within the framework of linked individual insurance, which he contracted or disposed of in favour of a third party by inter vivos act or on account of death, or which he transferred free of charge to a third person during his lifetime, are subject to reduction for their surrender value.

2. Claims of beneficiaries resulting from the deceased's individual linked pension plan with a banking foundation are also subject to reduction.

Art. 532

| III. On the order of reductions |

1. The reduction is applied in the following order until the reserve is reconstituted:

1. on acquisitions due to death resulting from the law;

2. on gifts made in contemplation of death;

3. on gifts inter vivos.

2. Gifts inter vivos are reduced in the following order:

1. Gifts made by marriage contract or by agreement on property which are taken into account for the calculation of reserves;

2. freely revocable gifts and benefits from tied individual pension plans, in the same proportion;

3. the other gifts, going back from the most recent to the oldest.

II

The modification of other acts is addressed in the appendix.

III

1 This law is subject to referendum.

2 The Federal Council sets the date of entry into force.

| Council of States, 18 December 2020 The President: Alex Kuprecht The Secretary: Martina Buol | National Council, December 18, 2020 President: Andreas Aebi Secretary: Pierre-Hervé Freléchoz |

Expiration of the referendum deadline and entry into force

1 The referendum period applicable to this law expired on April 10, 2021 without having been used.[3]

2 This law enters into force on January 1, 2023.[4]

| May 19, 2021 | On behalf of the Swiss Federal Council: The President of the Confederation, Guy Parmelin; The Chancellor of the Confederation, Walter Thurnherr |

Annex

(ch. II)

Amendment of other acts

The acts mentioned below are amended as follows:

1. Federal Law of 18 June 2004 on Partnership[5]

Art. 25, para. 2

Repealed

Article 31, paragraph 2

2. Unless otherwise stipulated, the partners lose all benefits resulting from provisions in respect of death:

1. at the time of the dissolution of the partnership;

2. at the time of death if a dissolution procedure resulting in the loss of the surviving partner's reserve is pending.

2. Law of 25 June 1982 on occupational old-age, survivors and disability insurance[6]

Article 82 Equivalent treatment of other forms of social protection

1. Employees and the self-employed can also deduct contributions allocated exclusively and irrevocably to recognized forms of social protection considered equivalent to occupational pension plans. The following are considered as such:

a. Individual linked pension plan with an insurance institution;

b. Individual pension plan linked to a banking foundation.

2 The Federal Council determines, with the collaboration of the cantons, to what extent the deductions referred to in paragraph 1 are permitted.

3. It establishes the terms and conditions of recognized forms of pension provision, in particular the circle and order of beneficiaries. It determines the extent to which the policyholder may modify the order of beneficiaries and specify their rights; the provisions made by the policyholder must be in writing.

4. Beneficiaries of a recognized form of social protection have a specific right to the benefit that this form of social protection entitles them to. The insurance company or banking foundation pays the benefit to the beneficiaries.

[1] FF 2018 5865

[2] RS 210

[3] FF 2020 9617

[4] The decision to bring it into force was subject to a simplified decision procedure

on 17 May 2021.

[5] RS 211.231

[6] RS 831.40