In the context of a succession, the sale of a business, the tax consequences can hold unpleasant surprises.

A skilful structuring makes it possible to carry out a succession, sale of company exempt from taxes or at least optimized on the tax plan.

The choice of the legal structure of a company is not often taken into account from the start of the activity. It is not uncommon to find that it is at the time of the sale of the latter that people begin to be concerned and it is unfortunately often too late to act and make the changes necessary for an advantageous final taxation,

Consequently, a large number of owners of small SMEs for whom this sale often represents the capital used to finance their retirement realize that once the taxes and duties have been paid, the balance will not be enough to achieve their goal.

If the legal structure of the seller is a sole proprietorship or a general partnership, thecapital gain from a sale of the company (ie the difference between the price paid by the buyer and the book value of the company) will besubject to the income tax and social insurance in addition to other income in the year of the sale, which is equivalent, depending on the private taxation of the person concerned, to charges of up to 50% of the sale profit.

Taxation when selling a business in Switzerland?

The tax rate on the sale of a business can vary between 0% and 50% depending on the structure of the transaction.

The elements that determine this rate are:

The legal structure of the Seller (ie SA, Sarl or partnership)

Buyer's legal structure

The taxation of a business transfer will be different if the structure of the seller and/or buyer is a partnership (ie sole proprietorship or general partnership or a capital company (ie SA or Sarl

2 - Potential taxes when selling a business?

1. Taxes on the capital gain on the sale of a company (ie for partnerships) 2. Indirect partial liquidation (ie for SAs, Sarl) 3. Transposition (ie for SAs, Sarl)

These taxes can be avoided with the right legal structuresand tax and financial preparation upstream of a business transfer transaction.

3 - Minimize taxation when selling a business?

It is essential and essential to put in place the right legal structures from the start!

A financial preparation upstream can allow you to avoid paying any tax!

Prepare the legal and financial structure ahead of the sale to minimize taxation when selling a business.

Negotiate the legal structure that the buyer will use to buy you out, as this may trigger other taxes (eg indirect partial liquidation)

The Swiss tax authorities may require 5 years before recognizing your new structure if necessary!

4 - Howto avoid capital gains tax?

The capital gain from the sale of a company or the capital gain from the sale of shares in a holding company will not be taxed in the same way depending on the legal structures of the parties to the transaction. A corporation (ie SA, Sarl) will be exempt from capital gain while a partnership will be subject to this tax.It is therefore important to transform your business into a capital company in the event of the sale of a business with a significant capital gain.

If the legal structure of the seller is a sole proprietorship or a general partnership, the capital gain on a sale of a company (ie the difference between the price paid by the buyer and the book value of the company) will be submitted and assimilated like an income tax.It will also be necessary to add the social charges (10%) which will also have to be paid.

Sole proprietorship and general partnership are therefore inadequate structures for minimizing the tax on the sale of business shares. One of the solutions to this situation is to transform the partnership into a capital company (ie SA or Sarl). This must be done 5 years before the actual sale of the company for the tax authorities to recognize this new structure. Selling your company with the lowest possible taxation must therefore be done with another legal structure.

CONCLUSION – PARTNERSHIPS ARE AN INADEQUATE FORMAT AT THE TAX LEVEL FOR THE TRANSMISSION OF BUSINESSES IN SWITZERLAND

Capital company – SA or Sarl

A capital company (ie SA or Sarl) benefits from an exemption from capital gains tax in Switzerland.

This means that no tax has to be paid on the capital gain of the shares/shares of the company when the SME is sold.

However, there is a situation where taxes must still be paidon the capital gain.If the seller holds the company privately and the buyer is a legal person (ie a company), this may lead to"indirect partial liquidation" which may generate tax payments after the sale (ie as described below). below).

B1. The buyer is a natural person

If the company being sold is a capital company held by a natural person in a private capacity and the buyer is also a natural person, no tax will have to be paid on the capital gain from the sale of the company. Taxation on the sale of a business is therefore not an issue in this case.

B2. The buyer is a legal person (ie company)

If the company for sale is a capital company owned by a natural person and the buyer is a legal person, two elements may apply: the "Transposition" and the "Indirect Partial Liquidation"

.

"Indirect partial liquidation" stipulates that taxes may be required from the seller after the sale of the company in the event of the presence and distribution within 5 years of excess reserves (eg large cash reserve in the company) in the company sold.

In this situation, capital gains are considered taxable income (and no longer exempt).

In order to avoid being in this business sale tax situation, transaction structures can be put in place by merger and acquisition advisors.

B2.1. What are the conditions for being in an indirect partial liquidation situation?

The sale involves a stake of at least 20%.

The transfer of shares leads to their passage from the private fortune of the seller to the commercial fortune of the buyer.

There are distributions of excess reserves (eg dividend greater than annual net income) within 5 years after the sale of the company

B2.2. Transposition, how does this impact the tax on the sale of a company?

Transposition is the act of transforming taxable (excess) reserves into non-taxable reserves.

As an example, imagine that a company has 100 of taxable excess cash and the new owner replaces this cash with a financial participation of another company. This transaction would allow the initially taxable amount (ie cash) to be replaced by a non-taxable amount (ie the new financial participation).

To compensate for this mechanism, the tax administration taxes this type of "transposition" as returns of fortunes. In order to avoid being in this tax situation, transaction structures can be set up by merger and acquisition consultants for SMEs.

C – Capital company – Real estate company SA or Sarl

A real estate company (SI) in Switzerland is a form of company, generally anonymous, whose corporate purpose is specifically the investment, construction and operation of buildings.

If the company for sale qualifies as a real estate company, the sale represents a transfer of economic ownership and lods and sales duties, as well as real estate gains taxes, are applicable.

6 – Donation subject to reservations

If shares are sold to a general partnership, to old or new members, the difference between the market value and the actual sale price (too low) may be considered a gift and gift tax may be levied accordingly.

Some cantons have a massive exemption from inheritance or gift tax in the context of business successions to tax-exempt recipients or heirs, such as e.g. the canton of Zurich which exempts at 80%.

However, depending on the canton, a period of between 5 and 15 years must be taken into account, during which the establishment must retain its corporate name or a majority stake must remain.

7 – Donations and legacies

In almost all cantons, gifts and inheritances to direct descendants are exempt from gift and inheritance tax.

If a succession within the family (in particular to children or grandchildren) is planned, the sole proprietorship, the participation in the partnership or the participations in capital companies can be given or bequeathed without taxation. The donor or the deceased does not suffer any tax consequences in this case either.

In principle, this exemption also applies to property taxes (lods duty and real estate sales and gains taxes), insofar as real estate is involved.

In the case of an internal succession within the family, the aspects of the law of succession (protection of the reserved part of the heirs who are not successors) must be taken into account. In some cases, a non-taxable division of the business into two (or more) parts of establishment is necessary for this purpose.

If the succession within the family should not be carried out free of charge, but facilitated by a reduced sale price, the company can be "lightened" in two ways: on the one hand, if this also turns out to be less attractive on a tax plan, by the withdrawal of cash useless for the operation of the company or, on the other hand, by the repurchase of own shares (up to 10%) at their market value, which must be resold within a period of 6 years.

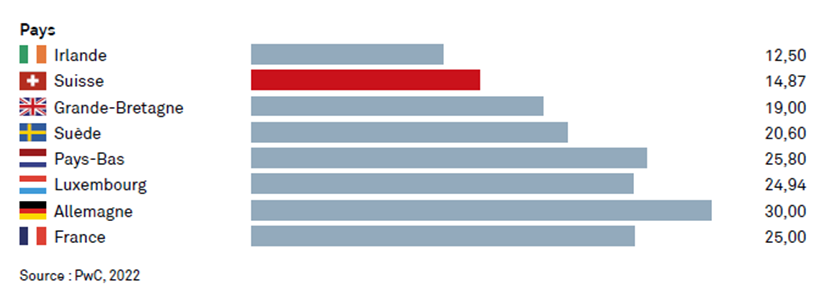

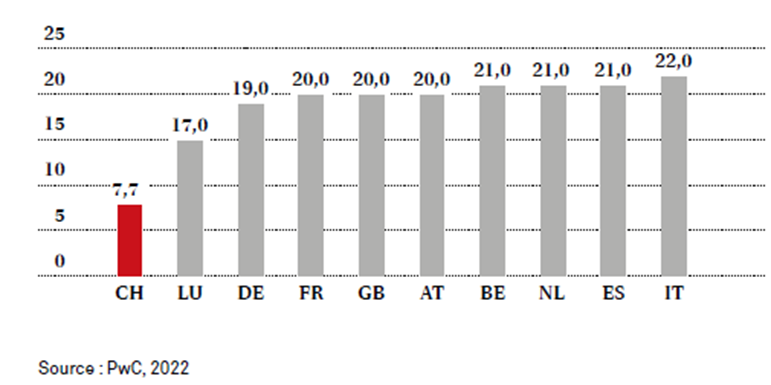

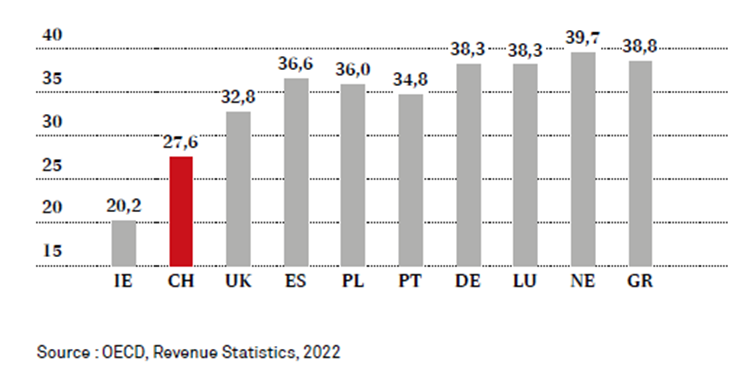

For reminder and information

Corporate tax in Europe

VAT in Europe

Tax shares in Europe

Taxes and contributions to social insurance 2020 in relation to GDP (in %)

The company law amended on January 1, 2023 has advantages and some potential pitfalls for financial institutions.

The share capital can be denominated in EUR, GBP, USD or JPY as long as it is the most important currency with regard to the company's activities.

Adopted by Parliament in June 2020, the reform of public limited company (SA) law entered into force on 1 January 2023. The new provisions aim in particular to relax the rules on capital and the foundation and to allow theformation of capital -shares in foreign currency.

In accordance with the timetable set by the Federal Council, the revision of public limited company law, materialized through amendments to the Code of Obligations (CO) and the Ordinance on the Commercial Register (ORC), has been effective since 1 January 2023.

As part of the relaxation of capital and foundation rules, the reform introduces a new tool : the capital fluctuation margin.

Fixed upstream, this margin will allow the board of directors to increase or decrease the company's capital for a maximum period of five years.

In addition, it will now be possible to establish a company's share capital in certain approved foreign currencies.

However, cryptocurrencies are excluded.

The reform also enshrined the provisions on excessive remuneration in the law. The Federal Council's Ordinance Against Excessive Remuneration in Public Limited Companies Listed on the Stock Exchange therefore lapsed and was repealed.

In addition to these novelties, the reform also contains provisions concerning the thresholds of gender representation in the management of large companies and an increase in transparency in the raw materials sector.

Companies have two years (until January 1, 2025) to bring their articles of association into line with the new law. In particular, they will have to make these changes in order to benefit from the capital fluctuation margin.

Four legal changes that may be of concrete interest to unlisted companies:

1. FOREIGN CURRENCIES

The share capital can be denominated in EUR, GBP, USD or JPY as long as it is the most important currency with regard to the company's activities. If the share capital is denominated in one of these currencies , the accounts must be presented in this same currency and, in this case, the equivalent values in Swiss francs must also be indicated.

SA law does not oblige the company to increase its share capital.

The share capital must be at least 100,000 francs, or its equivalent in foreign currency , when the company is incorporated .

Assuming that a company is founded with capital in EUR and that this currency devalues, the company will, in fact, have a share capital of less than 100,000 francs.

SA law does not oblige the company to increase its share capital. However, this situation may pose regulatory problems.

For asset managers, article 22 FinIA prescribes that the minimum capital of 100,000 francs “must be maintained at all times”.Finma could demand a capital increase under penalty of administrative measures.

2. INTERIM DIVIDENDS

A public limited company can distribute dividends to its shareholders during the financial year.

To do this, the company must draw up interim accounts and, if necessary, have these accounts revised according to the regime applicable to annual accounts (opting-out, restricted or ordinary audit).

The payment of interim dividends is of particular interest when the company is sold by its shareholders and it is supposed to be free of carried forward profits on the day of the sale.

3. SHAREHOLDER INFORMATION

In unlisted companies, shareholders representing together at least 10% of the share capital or votes may request in writing at any time information from the board of directors on the affairs of the company..

The board of directors is required to provide the information within four months. The new right thus allows shareholders to obtain information on the progress of business without having to wait for a general meeting.

4. GENERAL ASSEMBLY

The concrete procedures for holding the general meeting are extended.

General meetings can now be held (i) on several sites simultaneously with live transmission between the sites, (ii) without a physical meeting place (videoconference only) if the articles of association so provide, or (iii) abroad if the statutes so provide.

The Trade Register refusing articles of association that do not comply with the law in force at the time of the requisition for registration. n conclusion, since January 1, 2023, the adoption of new bylaws presents specific challenges; professional advice may be useful in this context.

An intermediate solution to the general power of attorney

Report :

With the evolution of medicine, life expectancy always lengthens a little more, on the physical level, but this evolution rarely follows the same curve on the mental level.

After a certain age, loss of memory and other mental faculties become commonplace.

The problem lies in the fact of no longer having the ability to realize it when it happens and not necessarily wanting to give immediate “general power of attorney” to these heirs or advisers when the ideas are still clear.

The need for future protection being obvious, the mandate on grounds of incapacity represents a good intermediate solution.

Mandate due to incapacity

A power of attorney is a legal document with which you can settle your representationin case of incapacity to discern.You will thus avoid a curatorship instituted by the State .

The mandate for reason of incapacity was introduced with the new law on the protection of adults in 2013 and constitutes an essential element of legal foresight.

Before drafting a mandate on grounds of incapacity, it is first necessary to understand what incapacity of discernment is.

What is the incapacity of discernment?

The Swiss Civil Code defines the capacity for discernment as follows: "Any person who is not deprived of the ability to act reasonably because of his young age, mental deficiency, psychic disorders, drunkenness or other similar causes, is capable of discernment within the meaning of this law.

Loss of ability to discern can be temporary or long-term . A temporary loss of judgment can occur, for example, after an accident or as a result of drug addiction. Typical cases of permanent disability are dementia or severe mental handicaps.

Who decides on the inability to discern?

The inability to discern is rarely total and must be assessed individually.

Since the introduction of the new Adult Protection Act in 2013, the Child and Adult Protection Authority (APEA) is responsible for assessing capacity.One of the main tasks of the APEA is to decide on the measures to be taken to protect or support a person who has become incapable of discernment.

The APEA assesses cases after receiving a report.

Anyone can send a report to the APEA. Certain authorities, such as the police or social services, have an obligation to inform the APEA.

If no report is received by theAPEA, the latter will take no action.

When does a mandate for incapacity come into effect?

The mandate due to incapacity is not valid immediately after it is drawn up, but only in the event of incapacity for discernment, noted by the authority for the protection of children and adults (APEA). The APEA must examine and validate the mandate for reason of incapacity.It is only then, if the mandate is validated by the APEA, that the mandate due to incapacity comes into force.

What is the difference between a power of attorney due to incapacity and a general power of attorney?

The power of attorney is valid as soon as it is signed, whereas the mandate due to incapacity is valid only after the occurrence of the incapacity to judge and its observation by the APEA .

In addition, banks generally no longer recognize powers of attorney after the onset of incapacity.

What is the difference between a mandate for incapacity and an advance directive?

In case of incapacity of discernment, theadvance directivesregulate the medical measures . The mandate for reason of incapacity regulates personal, financial and legal questions. In the absence of advance directives, the mandatary designated in the mandate for reason of incapacity for personal assistance decides on the medical measures.

What form should a mandate for incapacity take?

The mandate due to incapacity is subject to a strict formal requirement. It must be either written and signed entirely by hand , or authenticated by a notary. Authentication is especially recommended if the person concerned is not able to write himself.

Mandate due to incapacity – General

Or drop it:

Keep your money order somewhere easy to find, ideally with other important documents.

Give a copy to the agent and inform him of the place where you deposited the original.

We recommend that you register the constitution and the place of filing of your power of attorney due to incapacity in the civil status register of your municipality. Some cantons also offer the possibility of filing the mandate with the adult protection authority.

What does the mandate on grounds of incapacity contain?

The mandate due to incapacity is divided into three areas: personal assistance, asset management and legal representation . However, legal representation is always linked to personal assistance and asset management.

Who should I appoint as proxy?

Family members are often designated, especially (adult) children. In some cases, however, this is not possible or is not desired – both by the principal and by the agents.The following conditions must be met:

Agents must have sufficient expertise. Even though they are allowed to use attendants, they take responsibility for your entire life and finances.

Representatives must be flexible and available: they must have the necessary time to take care of everything and be able to get there quickly. If your children are already very involved in their private and professional life or live too far away, this could become problematic in the long term.

When examining the mandate on grounds of incapacity, the authority for the protection of children and adults (APEA) attaches importance to ensuring that there are as few conflicts of interest as possible. . Depending on the situation, mandating an heir can therefore become debatable. For this reason, under no circumstances should you appoint as proxy a person who already manages your assets (banks, asset managers or trustees). Serious financial service providers refuse to be named as mandatary in a mandate due to incapacity.

The liability of a mandate due to incapacity can last for years, even decades. Your agents should therefore be younger than you.

The most important thing is that it is easy to find.

The authority for the protection of children and adults (APEA) does not bother to seek a warrant for reasons of incapacity in the event of a report.

We therefore strongly advise against depositing your money order in a safe, in a bank or other.

However, the APEA is obliged to check in the register of the civil status office whether a mandate for reasons of incapacity has been entered.

We therefore recommend that you register your mandate due to incapacity with the civil status office of your place of residence.

Please note that you cannot file the mandate at the civil status office. However, you can indicate the place of filing on the form provided to you by the civil status office.

After having gone through the different stages of buying a house, from the search for the property, the visit, the choice, the negotiation of the price and the signing of the purchase contract, it is time to sign the deed.

What you need to consider before making a deed of sale.

The deed of purchase/sale (Escritura de um imóvel)

The notarial deed is the act by which the purchase and sale of real estate is established. It is carried out by means of a contract and constitutes the last phase of the whole process.

Normally it is preceded by the contract of promise of purchase and sale, where a value is paid that proves the interest in buying the property. ( **Information at the end of the file)

In this document, a deadline is stipulated, followed by the completion of the act, if the buyer so wishes.If the buyer does not wish to continue the transaction, he loses the right to the value of the deposit.(Deposit = O sinal)

On the day of the deed, the presence of both parties (buyer and seller) is mandatory in order to be able to sign it. The document is signed in front of a competent element who certifies the fulfillment of the law, thus testifying to the purchase and sale of the property. This body will have to verify and prove the identity of the two parties.

The deed of sale and mortgage consists of two moments:

Purchase and sale contract, which corresponds to the moment when the buyer becomes the legal owner of the property

If the house is purchased with a mortgage loan, an over-the-counter contract is drawn up, where all the steps concerning the loan are defined. It is only then that the bank releases the amount requested by the client for the purchase of the house.

Required documents

Civil and fiscal identification documents of stakeholders;

Promissory contract for the purchase and sale of property

Caderneta Predial Urbana or Application for registration of property in the matrix (Model I of IMI) issued by the Tax and Customs Authority

User license

Technical sheet of the building

Energy certificate

Certificate of content

Infrastructure Certificate

Mortgage deeds

Certificate of toponymy

Payment of the IMT (municipal property transfer tax).

Payment of stamp duty.

Where to have the deed drawn up (in person and online)

All deed costs are normally borne by the home buyer. There is no exact value that can be attributed to this process, as it depends on a series of factors, namely:

Purchase price of the house;

Whether it is a first or a second residence;

Expenses related to the payment of stamp duty on the transaction;

Stamp duty on credit;

Registration of the deed;

Fees with home loan, registry or notary services;

Costs associated with the payment of the IMT (IMT = value of the deed or value of the wealth tax (the higher of the two) x rate to be applied – part to be deducted. The IMT rates can be consulted on the portal financial ;

Place where the document will be drawn up.

Registration of the deed

Fees with CASA Pronta, Land Registry or Notary Services Costs associated with paying IMT (IMT = Deed Value or Wealth Tax Value (whichever is greater) x Rate to apply – share to be deducted IMT rates can be viewed on the financial portal;

Registration deadlines

It may take more or less time, depending on how long it takes to complete the various stages of buying and selling a property.

Generally and as an indication:

Obtaining Certificate of Title or Land Registry Certificate – 5 to 20 days;

Residence permit – 7 to 30 days;

Contract of promise to purchase and sale – 7 to 30 days;

Signature of the deed – 14 to 90 days;

Conclusion of the case in order to obtain the certificate of title and the certificate of the land registry

1 week to 1 month to receive the residence permit if the seller does not have one

1 week to 1 month to negotiate the terms of the promissory contract

2 weeks to 3 months to sign the deed and pay the balance to the seller

Registration at the land registry office after the deed – 30 days.

Types of real estate deeds

There are several types of acts, which differ according to the objective and the type of transaction. Below and in full

Deed of purchase and sale – the most common and best known;

Deed of purchase and sale with recourse to a financial institution – equal to the previous one but with bank intervention, due to the need for credit;

Deed for inherited property – the deed is usually carried out in the bodies mentioned above. The property must be in your name to be able to sell it. It is important to address this point before selling an inherited house;

Deed for a property under construction – A deed is signed between two parties and can be a bargain as it is usually a cheaper purchase, the property is new and you have more time to plan. However, it also has its drawbacks, the works may not be completed or may be completed later than expected and the finishes may be different from what you had envisaged;

Deeded ownership – the process is the same but there is no associated property value, in other words there is no cost to the buyer when purchasing the property. property ;

Deed of Property Exchanged – the deed consists of the exchange of properties and may or may not have associated values, depending on the value of the properties. If they have different values, the party that owns the asset with the lower value will have to pay the remaining value.

Promise of sale and purchase contract

(Contrato de promise de compra e venda)

CPCV. This is sure to be an acronym that many people will be familiar with. We are talking about the promise of sale contract, which is fundamental when buying a house, both for the current owner and for those interested in buying the property.

Constituting the first phase of the process of buying a property, the CPCV is very useful for those who want to buy a house. Although not mandatory , it is the mechanism used to formalize the intent to buy by the prospective buyer and to sell by the prospective seller.

In addition to offering great protection to the contracting parties , particularly in relation to situations of default of payment, it makes it possible to exclude other interested parties from purchasing the property.

What are the advantages of signing a CPCV?

By signing a CPCV, the contracting parties guarantee the validity of the contract until the signing of the public deed, stipulating their rights and duties, the date of conclusion of the final contract, the agreed values and the remaining clauses to be included in the future contract.

The promissory contract is even more advantageous in the case of the purchase and sale of real estate since, between the moment the parties decide to contract and the signing of the final contract, the conditions necessary for the public deed may not be fulfilled.

For example, in the event that the buyer does not have the necessary value to acquire the property, there will be the waiting time for the approval of the housing loan by the bank, or if the property is still under construction or does not have a housing permit, it is useful to sign a CPCV. This contract makes it possible to formalize a negotiation link between the contracting parties.

In addition, the promissory contract provides greater legal certainty in the relationship between the promissory seller and the promissory buyer, as it defines the consequences in the event of late payment or breach of contract by the parties.

The deposit(Sinal): What is it for?

Typically, in preliminary sales contracts,the promisor buyer pays a certain amount of money to the promisor seller as an advance(Sinal) or principal payment of the price of the good.This amount is called a deposit, according to article 441 of the Portuguese Civil Code.In the event of execution of the promissory contract, the deposit is included in the payment due when it coincides with the latter, in the light of article 242, paragraph 1, of the Portuguese Civil Code.

What happens if the promise contract is not fulfilled?

The consequences of the breach of the contract, promise of sale, can be defined by the parties to the contract. If the parties do not stipulate it, the general regime of article 442 of the CC applies:

If the non-compliance is due to the buyer of the promise, that is to say the party who delivered the deposit, this will be abandoned in favor of the counterparty;

If the non-compliance is the fault of the promising seller, that is to say the party who received the deposit, this must be refunded in duplicate.

If there is delivery of the property to which the promised contract refers, the promising buyer may choose, instead of returning the double deposit, to receive the current value of the property, at the time of the breach, less the agreed price, plus the deposit and the part of the price which has been paid. This solution, enshrined in No. 2 of Article 442 of the Civil Code, aims to avoid unjustified enrichment of the defaulting party. Otherwise, double depositing could be advantageous and therefore defaulting would also be advantageous.

As stated in Section 830, breach of the promissory contract also gives the non-defaulting party the right to seek specific performance of the contract. Thanks to this mechanism, the debtor is substituted in the execution and the creditor obtains the satisfaction of his right by legal means, thus constituting the definitive contract. It should be noted that the current legislation presumes that the existence of a deposit eliminates the possibility of a specific performance of the promissory contract in the light of the provisions of Article 830(2) CC. a rebuttable presumption.

The “chain carryover” of tax on real estate gains is based on the harmonized tax law of the cantons and municipalities.

By “chain deferral” we mean the (theoretical!) possibility of deferring the tax on real estate gains indefinitely based on different constituent elements of the deferral chained together.

Real estate gains tax

In the event of the alienation of buildings, the capital gains are subject to tax on real estate gains. This results in a gross profit insofar as the product exceeds the investment costs (acquisition price or other value replacing it, expenses) (art. 12 al. 1 LHID). According to the cantonal arrangement of tax law on real estate gains, certain deductions may be made on the gross profit.

The law assimilates several other legal acts (art. 12 al. 2 LHID) to the real change of ownership under civil law, which constitutes the most important case of application. One thinks, for example, of the sale of shares in a real estate company (“economic transfer”), the transfer of a building from private wealth to commercial wealth (“change of system”) or the creation of legal servitudes private on a building.

The decisive parameters for the calculation oftax, such as "income", "investment costs"and "replacement value", are legal concepts which are not specified by the law ofharmonization.

On the other hand, the notion of"replacementbuilding" is considered to be prescribed by theharmonization . On the whole, the Confederation therefore leaves the cantons and municipalities a certain leeway in defining the concept.

In the last 25 years since the entry into force of the harmonization legislation, haveexperienced an astonishing diversity of practices, particularly with regard todeferredtaxation.

As long asacantonal or communal practice is not thesubjectof proceedings before the Federal Court, it remains uncontested.Federal law does not provide foranyother “instrument ofharmonization”.

Thisisthe reason why it is possible that the tax base(the gross profit) varies fromonecanton toanother, despite the facts being identical in themselves , and not only because of the different scales.

For the deferral or the transfer of the real estate gain in another canton, it is therefore decisive to know in which canton the amount of the deferred real estate gainisdetermined.As we will see below, the deferred profitisalways determined in the canton where thebuildingis sold.This canton applies its own law.

Deferred from taxation

The deferred tax suspends the calculation of the increase in value operated on the building, although there has been a change of owner or a similar event.

Deferral of taxation is therefore an exception to the general principle of realization. The legal transaction is somehow treated as if the gross profit had not (yet) been realized.

Deferral of taxation can only be granted by the cantons in the five cases expressly and exhaustively mentioned by the federal legislator in art. 12 par. 3 lit. a — e LHID. These are the following:

In the event of transfer of ownership by succession ( devolution of heredity, inheritance sharing, bequest), advancement of inheritance or donation (case of inheritance law);

In the event of transfer of property between spouses in connection with the matrimonial regime or in the event of compensation for extraordinary contributions by a spouse to the maintenance of the family (art. 165CC) or claims arising from the law of divorce, provided that both spouses agree (case of family law);

In the event of parcel reorganizations (case of forced transfer);

In the event of total or partial alienation of an agricultural and/or forestry property, provided that the proceeds of the alienation are used, within a reasonable time, for the acquisition of a replacement property operated by the taxpayer itself or for the improvement of agricultural or forestry buildings belonging to the taxpayer and operated by him. (scenario “agricultural replacement acquisition”);

In the event of alienation of the dwelling (house or apartment) having been used for the long term and exclusively for the alienator's own use, insofar as the product thus obtained is allocated, within an appropriate period, to the acquisition or construction in Switzerland of a dwelling serving the same purpose. (case of the acquisition of a replacement building).

These five scenarios generating the tax deferral are systematically subdivided into clearly defined groups of cases , in particular:

A group of replacement acquisitions ( Figure 4 and 5), a group in which the owner does not receive any consideration for the transfer of the property (inheritance law, ( number 1 ) a) or within the family framework ( family law, ( figure 2 ), as well as a group which includes transfers of buildings based on constraint (plot reorganizations, ( figure 3 ).

It is possible to distinguish two types.

In the first case, the tax subject remains the same, while the building “changes” (in particular for replacement acquisitions [ numbers 4 and 5 ]).

In the other case, the building is not affected and the modification takes place via the exchange of the tax subject (in particular in the event of transfer of ownership between spouses or transfer of a deferred taxation is replaced by another tax deferral event, the corresponding conditions are also exchanged.

The reason why the federal legislator created the five scenarios, thus introducing the deferral of taxation, lay in important reasons of economic, social and social (privileged) policy.

In the event of a change of ownership, the cantons and municipalities are obliged to temporarily waive taxation of the gross profit. The principle is in a way the following: “not now, but later”.

Due to the exhaustive enumeration, the cantons and municipalities are also not authorized to create other scenarios as events giving rise to deferred taxation. Building as a donation, p. ex. ( digit 1 or 2 ). As part of the systematization, it should be borne in mind that each case has different conditions that must be met for the tax deferral to be granted.

Delimitations

Deferral of taxation must be distinguished from exemption ; the two legal institutions present important conceptual differences: the tax deferral lasts until the privileged reasons disappear.If the reason for the deferred taxation disappears or if all the conditions of a specific scenario are no longer met, there is taxation and the "profit on the capital gain" on the building constitutes the object of the tax. 'tax.

Taxation therefore remains possible after years of deferment.

On the other hand, in the case of tax exemption, the right to tax disappears from the moment the conditions are met and subsequent taxation is no longer possible after several years – which can be illustrated using the formula “not now, not later”.

It should also be specified that the deferment does not constitute an event giving rise to the reminder of tax within the meaning of art. 53 LHID, since the removal of the tax deferral does not constitute a fact within the meaning of art. 53 para. 1 or 51 par. 1 let. a LHID: It is not imposed retroactively, which should have already been imposed at the time. Rather, it is about taxing when the reasons for deferring taxation disappear.

Replacement Acquisition Requirements

The concept of "replacement building" is defined in a binding manner for the cantons and municipalities by the harmonization rule of art. 12 par. 3 lit. d and e LHID. The cantons and municipalities cannot independently define the legal concept governed by federal law .

This is all the more fair since replacement acquisition is also authorized beyond cantonal borders.

On the other hand, it remains within the competence of the cantons to set the scales, rates and amounts exempt from tax (“social deductions”) (cf. art. 1 al. 3 2 sentence LHID).

Both the alienated original object and the acquired replacement object must be occupied as a "dwelling used durably and exclusively for the alienator's own use".

"Dwelling" means that the owners establish their civil or fiscal domicile instead of the property relocation.

By "dwelling used for the alienator's own use", we therefore only mean the main residence, while a secondary tax residence cannot be taken into account for the deferred taxation in the case of a vacation property. .

In the case of a two-year lease by a third party, the Federal Court decided that there was no longer any own use.

In principle, use by a third party (such as rental to third parties) therefore excludes own use.

In the event of a deferral after a replacement acquisition, it is therefore recommended to authorize at most short-term use of the building by a third party. Otherwise, the tax authority risks no longer considering the condition of “long-lasting and exclusive use for its own use” fulfilled and charging for it through real estate gains tax.

The Federal Supreme Court explicitly leaves open the question of the period during which the replacement acquisition must take place. The cantons can themselves set the duration of the "appropriate period" within which the replacement acquisition must take place.

Most cantons generally provide for a period of two to five years.The Federal Supreme Court then ruled that a difference of seven years between the sale and the replacement purchase was in any case no longer appropriate.

Moreover, the replacement acquisition can be carried out not only retrospectively, but also in advance. In this case, one speaks of an “early replacement acquisition”.

Tax-deferred gain transfer method

The transfer of the tax-deferred gain is based on two methods approved by the Federal Court.

Application of the "absolute method"

The “absolute method”. According to this provision, deferred taxation is granted only for the part of the profit invested in the acquisition of the replacement object after reuse of the investment costs of the object sold (and any third-party services) .

If the means allocated to the replacement object do not exceed the investment costs of the alienated building, the real estate gain is taxed in full.

In this case, there is no deferred tax on real estate gains. The profit is considered realized and not reinvested. The profit not reinvested is taxed immediately. Therefore, the tax deferral according to Art. 12 par. 3 lit. e LHID should only be granted if and insofar as the proceeds reinvested in the replacement building exceed the investment costs of the initial building.

Application of the “unitary method”

It becomes interesting that the deferred taxation of real estate gains takes place beyond the cantonal borders.

The question that arises is to know to which canton the fiscal sovereignty over the initial real estate profit is attributed.

In intercantonal relations, the Federal Court ruled in favor of the application of the “unitary method” while excluding the “division method”

Thus, the deferred gross profit (and therefore the latent tax substrate) is allocated as a whole to the canton of arrival in the territory of which the alienation of the replacement property occurs, without any other tax deferral..

Gross profits form one and the same tax object in the (last) canton of arrival, hence the designation “single method”.

The splitting method , also discussed in doctrine, according to which the last taxable gross profit is distributed proportionally between the canton of departure and the canton of arrival (or the cantons of arrival), finds no basis in federal law.

The Federal Court thus confirms that not only are latent reserves transferred to the other canton, but that jurisdiction and sovereignty in matters of taxation also change from one canton to another.

In other words: “not now, but later” means, from a procedural point of view, that only the taxation authority of the “last” canton must act, applying exclusively its own law.

From the material point of view, the entire last gross profit goes to the "last" canton alone; the other cantons receive nothing.

Deferred by change of tax subject

The second type of deferred, through a modification of the tax subject, includes the assumptions of inheritance law and family law (numbers 1 and 2).

The canton of location cannot, despite a change of owner under civil law, impose the capital gain on the transferred building. According to the case law of the Federal Court, the reserve of usufruct does not lead, from an economic point of view, to a result significantly different from that of the transfer of property under civil law in the event of death.

The Federal Tribunal thus underlined that Art. 12 par. 3 lit. a LHID expressly includes deeds of succession inter vivos ("advancement of inheritance") and even gifts based on the law of obligations.

With regard to the advancement of inheritance (which also applies to the donation) of a building, the Federal Court recently ruled that the tax deferral could also be invoked in the event of a mixed legal act. The “free” part must not exceed a certain threshold.

The “chain delay”

It is particularly interesting to know what happens to the extension of the tax deferral when an event giving rise to deferred taxation is followed by another event giving rise to deferred taxation, i.e. say when case groups are combined.

Example 3: Daughter C. receives a co-ownership share from her mother. As the apartment does not meet her own needs, she sells the co-ownership share for 700,000 fr. and acquires a replacement building for 850,000 fr.

Combination possibilities and limitations

The law on tax harmonization does not expressly provide whether an event giving rise to deferred taxation can be replaced by another event giving rise to deferred taxation.

As we have seen, the harmonized tax law of the cantons and municipalities only regulates the five cases of facts giving rise to deferred taxation listed exhaustively.

Given the principle of horizontal and vertical harmonization and the fact that the condition, existence and revocation of tax deferrals are of fundamental importance, the Federal Court considered that the possibility of combining these two elements is not than a matter of federal law.It follows that the cantons cannot provide for their own combination possibilities, which is fair, since the cantons and the municipalities cannot create new events giving rise to deferred taxation either.

As long as the uninterrupted attachment of a new element to the old constituent element of an event giving rise to deferred taxation is guaranteed and the latent tax burden is fully maintained, the taxpayer may, of his own free will, switch from one event giving rise to deferred taxation to another.

The Federal Tribunal thus denied establishing a fact or a link between the facts.

The change between the different events giving rise to deferred taxation is thus based on federal law and the different scenarios can therefore be combined in different ways.

Informative processing of the “deferred chain”

In the case of a somehow “infinite” chain deferral, it can be problematic that the deferred profitcanno longer be replenished after decades.

This becomes particularlydifficultwhen several replacement acquisitions have already taken place beyond the cantonal borders.

In this respect, it is important that the taxpayer is obliged to cooperate (in particular to inform) with all the tax authorities involved in the intercantonal replacement acquisition.

Then, the canton which grants the replacement acquisition (“canton of departure”) communicates its decision to the tax authority of the canton where the replacement property is located (“canton of arrival”).

These obligations to inform and inform aim to guarantee information on the reference values which define the amount of the real estate gain and the amount of the reinvestment.

It is only when the reference values are known that it can be determined, when applying the absolute method, whether and to what extent the tax deferral should be granted.

In addition, according to the case law of the Federal Court, there is a right to obtain a finding decision fixing the amount of the (deferred) real estategain.

In theinterestsof legal certainty, taxpayers would do well to have the extent of the tax deferment determinedassoonaspossibleafterthereplacementinvestment.To do this, thetaxauthority must, as wehaveseen, issue a decision in finding, which is subject to the ordinary legal and appeal procedures.

The end of the “chain delay”

The tax deferral ends when:

A requirement is not met or disappears within a case group (e.g. the replacement property is no longer used "permanently and exclusively" or a spouse does not accept the deferral during the transfer of a building in the matrimonial regime); or if switching to another case group fails (eg there is no replacement investment within an “appropriate time”); or a final disposition takes place.

At the end of the chain, the count must relate to the last real estate gain made.

Profits made previously and which are subject to the tax deferral are not taken into account.

In particular, there is no accumulation of all winnings ever made . The calculation is “completely normal”, that is to say on the basis of the gross profit obtained last, without any other tax deferral.

The taxation of real estate gains occurs, as we have seen, in the absence of another event giving rise to deferred taxation ("at the end of the chain"). The terms and conditions in force at that time (scale, tax base, etc.) are decisive

Any event giving rise to deferred taxation may be replaced by a similar or legal event giving rise to deferred taxation, without there being immediate taxation. Thus, a “slaloming” exchange between the various events giving rise to deferred taxation is also authorized.

Challenges arise in particular when events giving rise to deferred taxation occur in inter-cantonal relations.

According to the “unitary method”, the last canton of situation, that is to say the one in which there is no new deferred taxation, is authorized to tax the gross profit realized during the last alienation. , applying its own tax law. The documentation of chain tax deferrals is therefore of great importance, not least for this reason.

The global tax landscape is changing with repercussions for Switzerland and the companies based there.

According to the roadmap planned by the OECD and the G20 states, the first elements of a minimum tax should come into force on January 1, 2023.The Federal Council has therefore decided to implement the minimum tax through a modification of the constitution and to ensure, by means of a transitional order, that the minimum taxation can be introduced on January 1, 2024.Voters will be called upon to vote on this subject on June 23, 2023.Fiscally, Switzerland remains an attractive place for businesses and individuals alike, but with a view to the introduction of a global minimum tax on large companies, some cantons must prepare to tax large companies more. In view of the reforms envisaged by the OECD and the G20 countries, which plan to introduce a minimum profit tax rate of 15% for companies , the differences that exist between cantons which tax their companies low, such as Zug 11.85%, and Berne 21.04% which tax them heavily will decline. However, the minimum tax rate of 15% targeted by the OECD will only apply to companies with an annual turnover of more than €750 million.In French-speaking Switzerland, the cantons of Vaud and Geneva have set their corporate profit tax rate at 14%, Neuchâtel at 13.57%, Friborg at 13.87%, Valais 17.12% and Jura at 16%. %. Compared to the minimum rate of 15% planned by the OECD, the gap is not very high and these cantons will only have to make a slight adaptation to be in compliance with the rates planned by the OECD In German-speaking Switzerland , the canton of Zug is at the top of the ranking, with a rate of 11.9%, Nidwalden (12.0%) and Lucerne (12.2%). With a rate of 21.0%, the canton of Bern is at the bottom of the pack .

2022 profit tax rates in Switzerland In international comparison, companies are taxed low in Switzerland . Rates lower than those in low-tax cantons are only found in traditional offshore domiciles, in Guernsey, Qatar and a few countries in Eastern (southeast) Europe. Ireland remains Switzerland's main competitor in Europe. Internationally, large Swiss companies will also be subject to the same rules as those located in cities like Singapore, Hong Kong or Dubai, which will also have to increase their tax rate to 15%. There will therefore be fewer incentive factors which will encourage companies to move to such locations purely for tax reasons. For very large companies, tax competition between cantons will play a less important role as a factor in establishing themselves in the future. future. As for whether developments in corporate taxation will have consequences for personal taxation, only time will tell.

To provide the best experiences, we use technologies such as cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Failure to consent or withdrawing consent may negatively impact certain features and functions.

Functional

Always On

The storage or technical access is strictly necessary for the purpose of legitimate interest to allow the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of communication over an electronic communications network.

Preferences

The storage or technical access is necessary for the legitimate interest purpose of storing preferences that are not requested by the subscriber or user.

Statistics

Technical storage or access that is used exclusively for statistical purposes.Technical storage or access that is used exclusively for anonymous statistical purposes.Absent a subpoena, voluntary compliance by your Internet Service Provider, or additional records from a third party, information stored or retrieved for this sole purpose cannot generally not be used to identify you.

Marketing

Storage or technical access is necessary to create user profiles in order to send advertisements, or to track the user across a website or across multiple websites with similar marketing purposes.